Skip to content

About Us

Our Company

Meet Our Team

Careers

USDA OneRD Loans

USDA Business & Industry Loans | USDA B&I

Assisted Living Facility Loans

Commercial Real Estate Loans

Family Entertainment Center Loans

Food Processing Loans

Hotel & Hospitality Loans

Manufacturing Loans

Outdoor Experience Loans

Sports & Recreation Loans

Timber & Lumber Loans

Winery & Vineyard Loans

USDA Community Facilities Loans | USDA CF

College & University Loans

Healthcare Loans

Public Safety Loans

USDA Rural Energy for America Program | USDA REAP

Anaerobic Digester & Biomass Loans

Solar Energy Loans

Wind Energy Loans

SBA 7(a) Loans

Compare USDA OneRD & SBA 7(a) Loans

NAC & Veritex Community Bank | Partnership & History

Broker Program

Broker Program Portal

Tools & Resources

Blog

Borrower Stories

Geographic Eligibility Map

USDA OneRD Guidelines

Webinars

Contact

Apply for a Loan

Map

Search Icon

About Us

Our Company

Meet Our Team

Careers

USDA OneRD Loans

USDA Business & Industry Loans | USDA B&I

Assisted Living Facility Loans

Commercial Real Estate Loans

Family Entertainment Center Loans

Food Processing Loans

Hotel & Hospitality Loans

Manufacturing Loans

Outdoor Experience Loans

Sports & Recreation Loans

Timber & Lumber Loans

Winery & Vineyard Loans

USDA Community Facilities Loans | USDA CF

College & University Loans

Healthcare Loans

Public Safety Loans

USDA Rural Energy for America Program | USDA REAP

Anaerobic Digester & Biomass Loans

Solar Energy Loans

Wind Energy Loans

SBA 7(a) Loans

Compare USDA OneRD & SBA 7(a) Loans

NAC & Veritex Community Bank | Partnership & History

Broker Program

Broker Program Portal

Tools & Resources

Blog

Borrower Stories

Geographic Eligibility Map

USDA OneRD Guidelines

Webinars

Contact

Apply for a Loan

Map

Search Icon

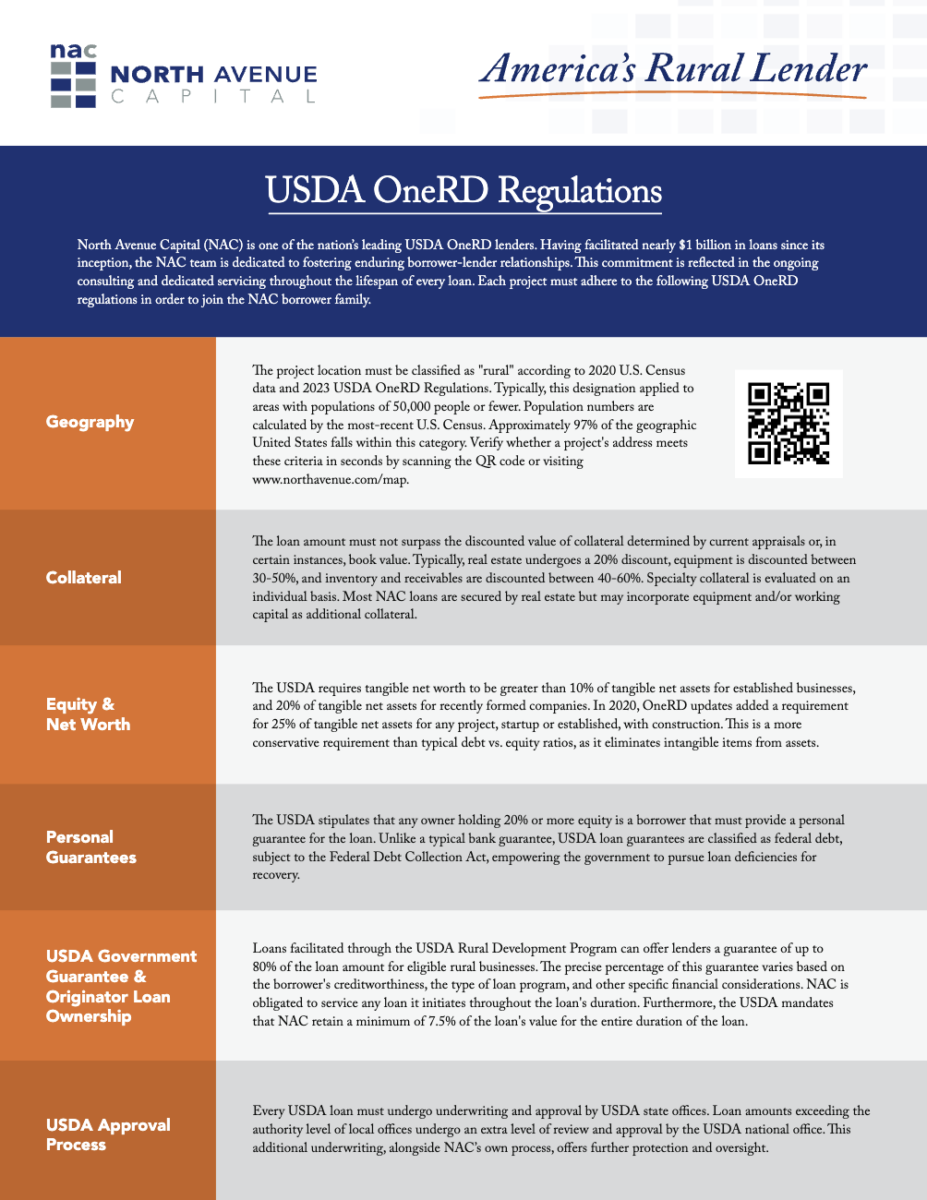

USDA Regulations

Download the USDA OneRD Regulations from North Avenue Capital

North Avenue Capital is one of the nation’s leading USDA OneRD leaders and dedicated to fostering enduring borrower-lender relationships.

Enter Search Query

Search for: